2023 was an intriguing year in that many indicators were flashing recession, yet the economy was resilient while inflation collapsed. We happily spend our time exhaustively analyzing data and mitigating risk, so our client partners can spend time enjoying their personal pursuits. The underlying data showed there was a tug of war between high fiscal stimulus totaling $1.65 Trillion (Inflation Reduction Act, CHIPS, Infrastructure) and tighter monetary policy as the Fed increased rates 1% to 5.25-5.5%.

In 2023, the S&P 500 recovered its losses from the prior year. A surprising result for the latest rolling twelve-month period. Few investors were expecting such a swift recovery amidst rising rates and the old adage, “Don’t Fight the Fed.” This is another humble reminder of our mantra that “the future is uncertain.”

This humility leads to creating client partner portfolios that have some semblance of balance to the Core Four economic environments while also investing in idiosyncratic strategies that are likely to generate returns regardless of the environment (shareholder activism, quantitative long/short, multi-strategy, distressed private opportunities, hedged credit, etc.). Our approach leads to greater peace of mind due to lower volatility, which produces fewer cognitive misjudgment errors. Not “selling at the bottom” or aggressively “buying at the top” results in our client partners reaching their long-term financial objectives.

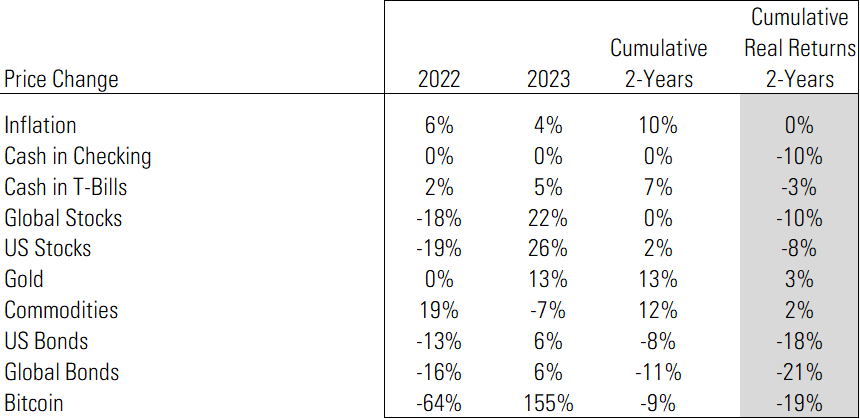

For instance, consider the cumulative performance figures for a broad selection of asset classes over the past two years beginning 1/1/2022. Of particular note, is the right-hand column, which displays “Real Returns” over the two-year period or put another way, returns after subtracting inflation. The only two asset classes with positive real returns were gold and commodities. Not only were these two asset classes positive vs. inflation but their performance was uncorrelated to most investors’ largest holding, US stocks. For instance, US stocks were down 19% in 2022 yet commodities were up 19% and gold was flat. This is an endorsement of diversification, not for a larger weighting in gold and commodities vs. stocks.

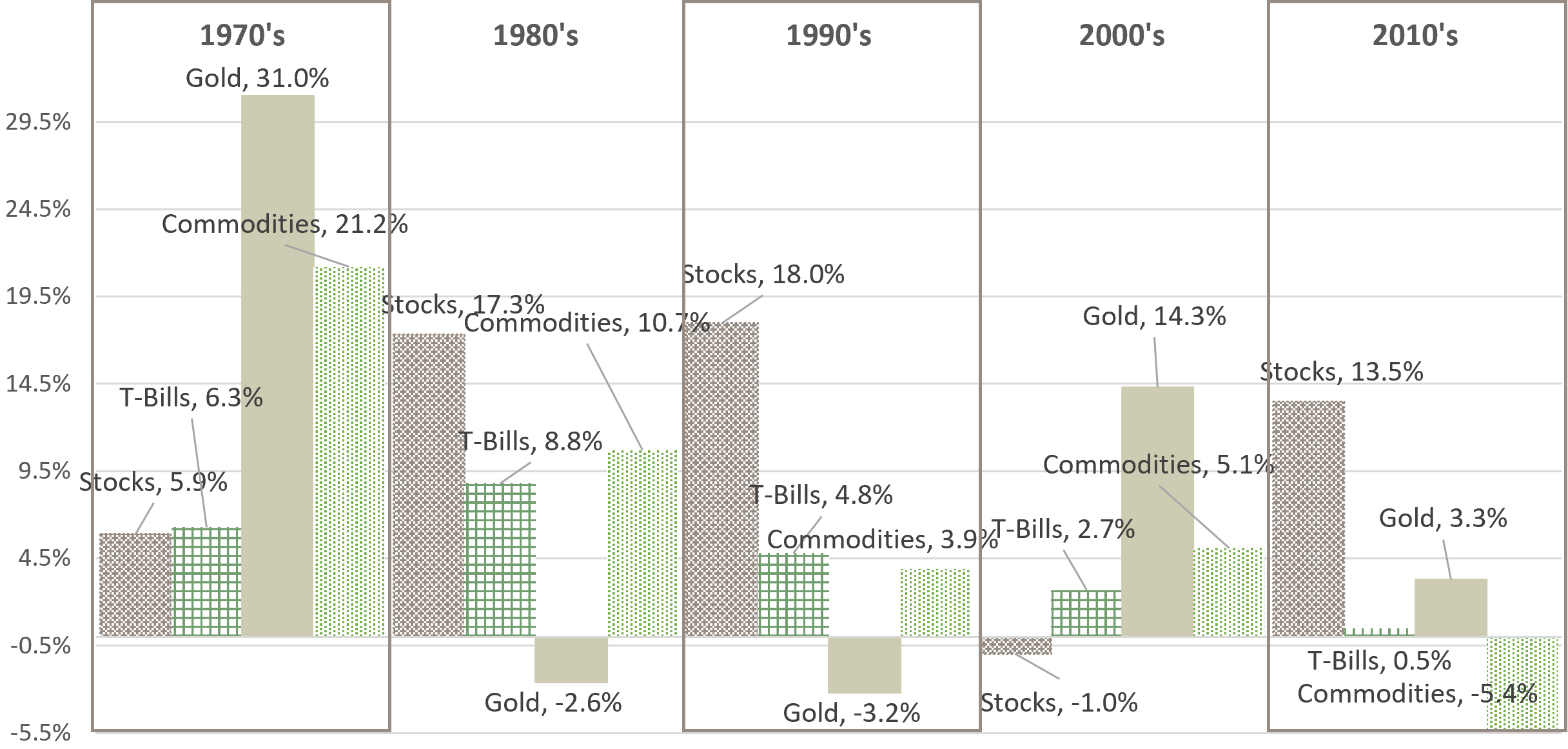

Zooming out further, consider the following chart showing annual returns by asset class over the past 5 decades. Let’s use commodities in the 1970’s to understand the chart data. For the 10 years in the 1970’s, commodities produced a 21.2% compounded annual return or $100 invested in commodities in 1970, grew to $683 at the beginning of 1980.

Now to the point, US stocks produced a negative “Real Return” in the 1970’s and 2000’s while gold and commodities drastically outperformed in those two decades. While this is an interesting observation, the challenging aspect of owning diversified investments is not the good times, it’s the long stretches of time, possibly years, when they underperform stocks. Gold languished for two decades after its bubble peak in 1980. Tactical adjustments matter too.

Excessive pessimism is not rewarded in financial markets in the long term. I am cautiously optimistic headed into 2024 with a greater degree of caution in the first half. This is due to difficult economic growth comparisons as we lap the superfluous fiscal spending binge of 2023. The Fed’s dot plot expects the Fed to cut rates 3 times over the coming year. I disagree, yet the path is uncertain.

If the economy is strong, no cuts are likely and interest rates remain “higher for longer” to suppress further inflationary bursts. In this scenario, a re-acceleration of inflation is likely at some point. However, if the economy falters and deflationary forces kick in, we could see the Fed funds rate go below 3% and new fiscal stimulus, sowing the seeds for the next inflationary up-cycle. The historical record of economic “soft landings” is largely non-existent, further reinforcing our approach to manage portfolio risks. Our view is that the current disinflationary forces are cyclical in what will be higher structural inflation in the current decade. For a review of our long-term view of inflation, please refer to our 2021 writings on our website: Inflation: Secular Analysis by Essential Partners

I appreciate your continued trust and support.

Investment advisory services offered through Essential Partners, LLC, an SEC registered investment adviser.

This presentation contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this presentation will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Essential Partners, LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.

Factual material is obtained from sources believed to be reliable and is provided without warranties of any kind, including, without limitation, no warranties regarding the accuracy or completeness of the material. This information is subject to change, and although based on information that Essential Partners, LLC considers to be reliable, it is not guaranteed as to accuracy or completeness. Any market data is provided “as is” and on an “as available” basis. Source information, such as security prices, dividend rates, etc., is obtained from independent financial data suppliers.