Market Backdrop: 1/1/2026 to 3/31/2026 Gold rose 8.4% during the quarter, with higher short-term volatility than the prior year The S&P 500 declined 4.4%, its weakest quarter since 2022 International developed and emerging markets finished the quarter higher, returning 3.0% and 3.8%, respectively, and continued to outperform the S&P 500 The U.S. dollar strengthened modestly, […]

The third quarter of 2025 will be remembered for new highs, noisy headlines, and a market that continued the themes established in the prior quarters. Equities: U.S. stocks set multiple all-time highs before finishing just below the peak. Gold: Continued its climb, ending the quarter near $3,900/oz. U.S. Dollar: Traded in a range but remains […]

We write on this Fourth-of-July weekend as unapologetic patriots who still believe American capitalism is the greatest compound-interest engine man has devised. Still, as stewards of our client partner’s capital, we need to assess the risks and opportunities both at home and abroad. The US markets entered the second quarter fairly strong, but were met […]

While we always perform rigorous analysis on the economic and market environment, we operate with the humility that the future is uncertain and investing is driven by expected returns and probabilities. Risk and tactical opportunities can be executed on the margin in benign environments and in periods of tumult, fat pitches do emerge (higher probability, […]

The future is uncertain is one mantra we live by at Essential Partners. For this reason, we humbly design portfolios that are resilient to the Core Four Economic Environments as defined by the rate of change in economic growth and inflation. Our client partner’s personal situation and objectives come first but the Core Four seeks […]

From time to time, we will feature investment topics we are researching in our quarterly memo. For this quarter, the topic is Private Debt, which we consider to be an attractive investment opportunity with current distribution yields of 10%. We like the combination of high current yield distributions, historically low default rates, consistent performance across […]

Are you planning on selling your business but face a large, painful tax bill? Do taxes prevent you from selling even though you want to lower your stress and risk? Have you already sold your business but have an earn-out or “rollover equity” that you plan to sell for a future taxable gain? Are you […]

I am a huge Patriot and a big fan of U.S. stocks over the long run. U.S. stocks are the largest holding for the vast majority my client partners. However, U.S. stocks have underperformed cash in 3 of the last 9 decades; 1930’s, 1970’s and 2000’s. A lost decade is unacceptable for my client partners […]

Is it possible for lower risk to lead to higher returns? How can the implementation of quality-based investment strategies also lead to large tax efficiencies? What if investing in high-quality stocks could yield higher returns with less risk while also being extremely tax-efficient? We believe in a globally diversified approach with some exposure to each […]

2023 was an intriguing year in that many indicators were flashing recession, yet the economy was resilient while inflation collapsed. We happily spend our time exhaustively analyzing data and mitigating risk, so our client partners can spend time enjoying their personal pursuits. The underlying data showed there was a tug of war between high fiscal […]

Are you aware that “high yield bonds” finally have “high yields” recently >9%? What are credit investments and what is the opportunity? Does it make sense to bother when I can get >5% yields in short-term U.S. Treasury bonds? If I own investments with high current income, should I own them in a taxable or […]

Are you charitably inclined? If not, no judgement here, but stop reading. We have other ideas for you. Do you have annual tithing commitments to your church? What is a Donor Advised Fund? Are you planning on selling your private business but face a large tax bill? Philanthropy can be an important strategic aspect of […]

What is an unsustainable capital structure? Translation: Too much debt. How have the Fed’s interest rate increases impacted private businesses with high debt levels? What is the opportunity for patient investors? One of the most well-known quotes from one of the greatest marketers (and investors) of all time… “You never know who’s swimming naked until […]

What is the “Money Illusion?” How can the concept of the Money Illusion relate to investment returns in the current environment? What is your framework to manage risk in periods when investment return interpretation can be distorted by the Money Illusion? The recovery of the S&P 500 in 2023 has been swift. Since the beginning […]

Have you considered the mindset and thought process differences between operating a business for personal cash flow vs. earning an investment return? Have you performed a comprehensive financial forecast for you and your family considering your financial situation post-sale? Do you understand your investment options and a range of investment returns? Is your nest egg […]

Why should I care about investing in Japan? That sounds risky! What is shareholder activism? How is the opportunity in Japan like Private Equity in the U.S. in the 1980’s? “I am delighted to have Berkshire Hathaway participate in the future of Japan.” – Warren Buffett I made my first investment in a Japanese stock […]

Are you planning on selling your private business but face a large tax bill? What is a Qualified Opportunity Zone or Qualified Opportunity Zone Fund? Do you understand how to increase your long-term tax efficiency while investing in real estate? “Taxes are killing us, but I don’t know all the strategies.” – Anonymous Pest Control […]

Does the changing landscape of estate tax exemptions concern you? Are you seeking a flexible and strategic approach to secure your estate for your beneficiaries? Does the idea of losing access to your financial resources worry you when considering estate planning strategies? Are you interested in reducing your estate tax liability while maintaining access to […]

David Senra is an animal and I love his podcast, “Founders.” Senra is authentically enthusiastic about studying historically significant founders and his pursuit makes me recall Charlie Munger’s thoughts on this process. “I make friends with the eminent dead.” – Charlie Munger The Founders podcast consists of Senra reading a biography of a founder, analyzing, […]

Does putting a large amount of your investments in a trust seem like too large of a commitment all at once? Are you comfortable giving investments and cash annually to your children without controlling how the money is utilized? Are you worried about losing control of your assets by putting them in a trust? Is […]

Are you planning on selling your pest control business but face a large, painful tax bill? Have you sold your business and rolled equity that you plan to sell for a gain? Are you aware of institutional investment strategies that could lead to >20 cents of tax savings on each dollar invested? Or substantially more […]

Do you know the true cost of holding excess cash in your business bank accounts? Would additional capital be helpful to fund your business growth while taking less risk? How many more team members could you hire (or not fire) if you earned more interest on your cash? Does your bank salesperson have any incentive […]

As of September 30, 2022, the current year is the worst start for bonds since 1926 as the overall U.S. bond market is down nearly 15%. While this is disappointing, it also creates a unique, once in a generation, tax loss harvesting opportunity. This strategy can reduce current and future taxes. Tax loss harvesting is […]

Do you have high, excess cash in your business cash account earning close to 0% interest while inflation is recently greater than 6%? Do you find traditional alternatives such as CDs or money market accounts similarly unattractive given interest rates 1% to 2% and long commitment periods greater than 1 year? Do you understand your […]

Which investment solutions that you own will perform well in an inflationary environment? At Essential Partners, we build portfolios for all types of economic environments, including rising inflation. Despite inflation being littered across the news and social media daily, the past 40 years have conditioned individual and institutional investors to not worry about inflation. This […]

What is your compass to traverse global financial markets and how does that translate to your portfolio? Do you own investments that perform well in all four economic environments? There are two core marcroeconomic variables that drive financial market changes; GROWTH and INFLATION. Consider a simple micro example as it relates to equities/stocks: Sales growth […]

Do you know that in 2 of the last 5 decades, stocks produced negative real returns vs. cash? What assets do you own that perform best in the decades when stocks perform worst? Do you own any assets that will perform well when inflation is high but economic growth is low? “Gold is money, […]

Investment portfolios that are balanced to various economic and inflationary environments will at times contain certain holdings with unrealized capital losses. Tax loss harvesting is a tactical portfolio strategy to sell these holdings to capture the capital losses, which can then be used to offset the capital gains realized elsewhere in the portfolio. Further, the […]

Do you know the true cost of your investment holdings? Does your salesperson/broker receive commissions? Does your salesperson’s firm capture any special distribution or marketing fees at your expense? Does your salesperson have sufficient training? Does your “robo-advisor” force you to hold too much cash? Warren Buffett’s partner Charlie Munger is famously outspoken regarding the […]

Do you have a disciplined process and documentation for your investment strategy? Does your salesperson/broker provide an Investment Policy Statement to set clear investment objectives, guidelines, and expectations? “Successful investment takes time, discipline and patience.” – Warren Buffett In our experience, no serious pension or endowment would invest without first creating an Investment Policy Statement. […]

Will your salesperson/financial advisor analyze investments they do not bring to you where they cannot earn fees or commissions? Has your salesperson/financial advisor ever thought your investment idea was a great idea if it meant you would be pulling the money from their control and fee structure? Has your investment advisor ever analyzed a company’s […]

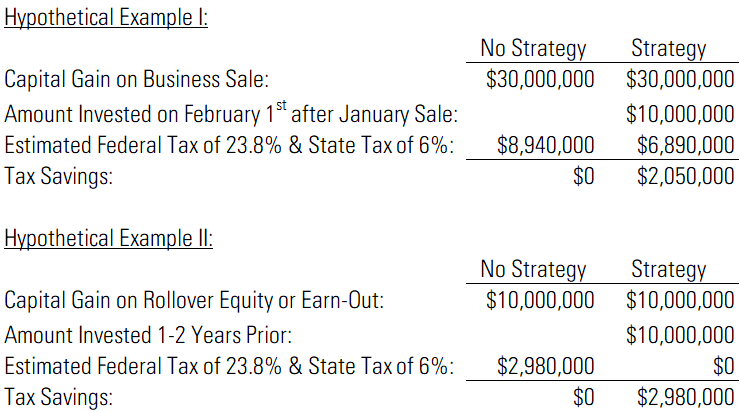

- Are you planning on selling your business but face a large, painful tax bill?

- Do taxes prevent you from selling even though you want to lower your stress and risk?

- Have you already sold your business but have an earn-out or “rollover equity” that you plan to sell for a future taxable gain?

- Are you aware of institutional investment strategies that target market-beating investment returns, yet can significantly reduce or eliminate your immediate capital gains tax burden? These strategies are not close to any “red line,” and your money is not locked into a trust, fake charity or insurance policy.

“I was maximizing the value of my business, so I didn’t think about tax strategy.”

- Anonymous Home Services Business Owner

Building a home services business inch by inch takes discipline, risk-taking, creativity, resilience, and many other skills…including expert employee relations skills. Imagine the first tax-day after you sell your business, and you give our wasteful government up to 1/3 or more of your hard-earned cash. That is an extremely painful thought and leads to less after-tax cash to invest or pay for your lifestyle.

If you do not spend your free time reading the Financial Analysts Journal or The Journal of Beta Investment Strategies, then you are most likely not aware of dynamic, tax-mitigation investment strategies. These strategies can lead to capital gains tax savings on a business sale while targeting market-beating investment returns. Further, the anticipated gains on rollover equity or an earn-out from a prior business sale can also be mitigated and likely with greater impact.

Essential Partners is not an M&A advisor and we do not prepare taxes. We are a wealth advisory firm that helps business owners pre- and post-sale across multiple dimensions including tax mitigation, investment management, trust & estate and cash flow planning while utilizing our Family Office Services.

For details, email us at info@essentialp.com, call 213-878-0075 or visit www.essentialp.com/contact-us/.

This presentation contains general information that is not suitable for everyone. This is not tax advice and you must consult a CPA. The information contained herein should not be construed as personalized investment advice. There is no guarantee that theviews and opinions expressed in this presentation will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Essential Partners, LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.