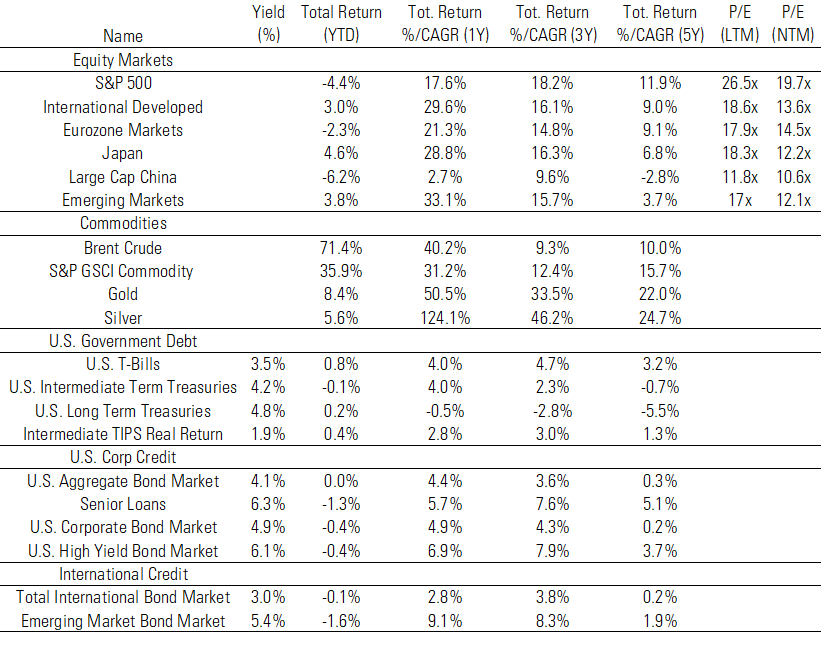

Market Backdrop: 1/1/2026 to 3/31/2026 Gold rose 8.4% during the quarter, with higher short-term volatility than the prior year The S&P 500 declined 4.4%, its weakest quarter since 2022 International developed and emerging markets finished the quarter higher, returning 3.0% and 3.8%, respectively, and continued to outperform the S&P 500 The U.S. dollar strengthened modestly, […]

The third quarter of 2025 will be remembered for new highs, noisy headlines, and a market that continued the themes established in the prior quarters. Equities: U.S. stocks set multiple all-time highs before finishing just below the peak. Gold: Continued its climb, ending the quarter near $3,900/oz. U.S. Dollar: Traded in a range but remains […]

We write on this Fourth-of-July weekend as unapologetic patriots who still believe American capitalism is the greatest compound-interest engine man has devised. Still, as stewards of our client partner’s capital, we need to assess the risks and opportunities both at home and abroad. The US markets entered the second quarter fairly strong, but were met […]

While we always perform rigorous analysis on the economic and market environment, we operate with the humility that the future is uncertain and investing is driven by expected returns and probabilities. Risk and tactical opportunities can be executed on the margin in benign environments and in periods of tumult, fat pitches do emerge (higher probability, […]

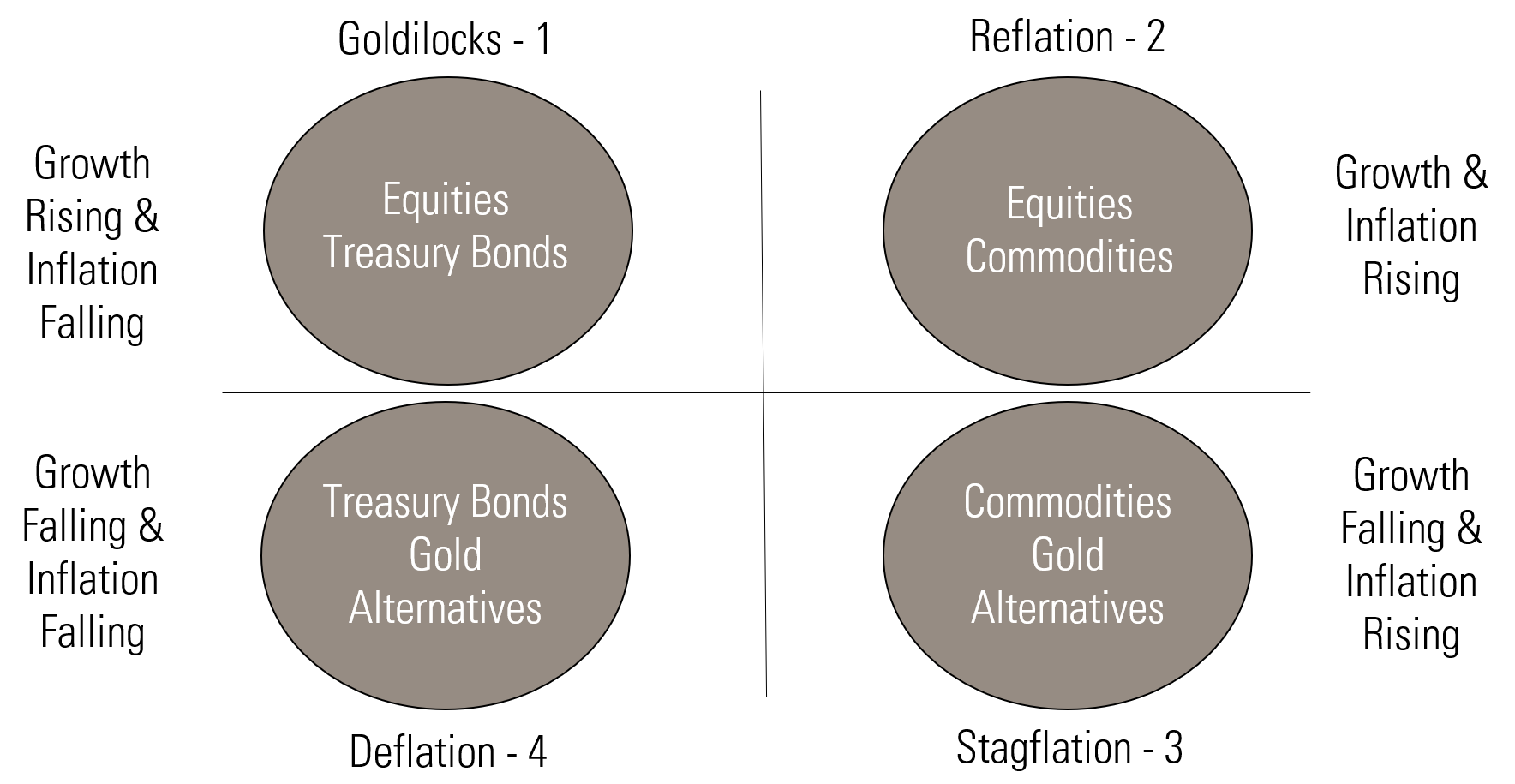

The future is uncertain is one mantra we live by at Essential Partners. For this reason, we humbly design portfolios that are resilient to the Core Four Economic Environments as defined by the rate of change in economic growth and inflation. Our client partner’s personal situation and objectives come first but the Core Four seeks […]

From time to time, we will feature investment topics we are researching in our quarterly memo. For this quarter, the topic is Private Debt, which we consider to be an attractive investment opportunity with current distribution yields of 10%. We like the combination of high current yield distributions, historically low default rates, consistent performance across […]

Are you planning on selling your business but face a large, painful tax bill? Do taxes prevent you from selling even though you want to lower your stress and risk? Have you already sold your business but have an earn-out or “rollover equity” that you plan to sell for a future taxable gain? Are you […]

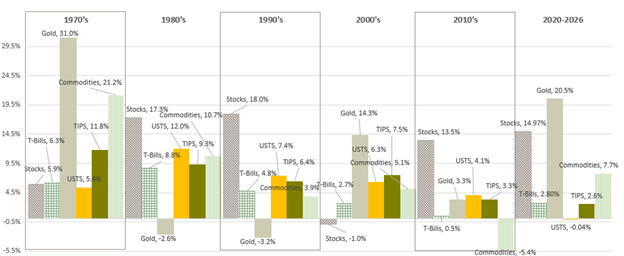

I am a huge Patriot and a big fan of U.S. stocks over the long run. U.S. stocks are the largest holding for the vast majority my client partners. However, U.S. stocks have underperformed cash in 3 of the last 9 decades; 1930’s, 1970’s and 2000’s. A lost decade is unacceptable for my client partners […]

Is it possible for lower risk to lead to higher returns? How can the implementation of quality-based investment strategies also lead to large tax efficiencies? What if investing in high-quality stocks could yield higher returns with less risk while also being extremely tax-efficient? We believe in a globally diversified approach with some exposure to each […]

2023 was an intriguing year in that many indicators were flashing recession, yet the economy was resilient while inflation collapsed. We happily spend our time exhaustively analyzing data and mitigating risk, so our client partners can spend time enjoying their personal pursuits. The underlying data showed there was a tug of war between high fiscal […]

Are you aware that “high yield bonds” finally have “high yields” recently >9%? What are credit investments and what is the opportunity? Does it make sense to bother when I can get >5% yields in short-term U.S. Treasury bonds? If I own investments with high current income, should I own them in a taxable or […]

Are you charitably inclined? If not, no judgement here, but stop reading. We have other ideas for you. Do you have annual tithing commitments to your church? What is a Donor Advised Fund? Are you planning on selling your private business but face a large tax bill? Philanthropy can be an important strategic aspect of […]

What is an unsustainable capital structure? Translation: Too much debt. How have the Fed’s interest rate increases impacted private businesses with high debt levels? What is the opportunity for patient investors? One of the most well-known quotes from one of the greatest marketers (and investors) of all time… “You never know who’s swimming naked until […]

What is the “Money Illusion?” How can the concept of the Money Illusion relate to investment returns in the current environment? What is your framework to manage risk in periods when investment return interpretation can be distorted by the Money Illusion? The recovery of the S&P 500 in 2023 has been swift. Since the beginning […]

Have you considered the mindset and thought process differences between operating a business for personal cash flow vs. earning an investment return? Have you performed a comprehensive financial forecast for you and your family considering your financial situation post-sale? Do you understand your investment options and a range of investment returns? Is your nest egg […]

Why should I care about investing in Japan? That sounds risky! What is shareholder activism? How is the opportunity in Japan like Private Equity in the U.S. in the 1980’s? “I am delighted to have Berkshire Hathaway participate in the future of Japan.” – Warren Buffett I made my first investment in a Japanese stock […]

Are you planning on selling your private business but face a large tax bill? What is a Qualified Opportunity Zone or Qualified Opportunity Zone Fund? Do you understand how to increase your long-term tax efficiency while investing in real estate? “Taxes are killing us, but I don’t know all the strategies.” – Anonymous Pest Control […]

Does the changing landscape of estate tax exemptions concern you? Are you seeking a flexible and strategic approach to secure your estate for your beneficiaries? Does the idea of losing access to your financial resources worry you when considering estate planning strategies? Are you interested in reducing your estate tax liability while maintaining access to […]

David Senra is an animal and I love his podcast, “Founders.” Senra is authentically enthusiastic about studying historically significant founders and his pursuit makes me recall Charlie Munger’s thoughts on this process. “I make friends with the eminent dead.” – Charlie Munger The Founders podcast consists of Senra reading a biography of a founder, analyzing, […]

Does putting a large amount of your investments in a trust seem like too large of a commitment all at once? Are you comfortable giving investments and cash annually to your children without controlling how the money is utilized? Are you worried about losing control of your assets by putting them in a trust? Is […]

Are you planning on selling your pest control business but face a large, painful tax bill? Have you sold your business and rolled equity that you plan to sell for a gain? Are you aware of institutional investment strategies that could lead to >20 cents of tax savings on each dollar invested? Or substantially more […]

Do you know the true cost of holding excess cash in your business bank accounts? Would additional capital be helpful to fund your business growth while taking less risk? How many more team members could you hire (or not fire) if you earned more interest on your cash? Does your bank salesperson have any incentive […]

As of September 30, 2022, the current year is the worst start for bonds since 1926 as the overall U.S. bond market is down nearly 15%. While this is disappointing, it also creates a unique, once in a generation, tax loss harvesting opportunity. This strategy can reduce current and future taxes. Tax loss harvesting is […]

Do you have high, excess cash in your business cash account earning close to 0% interest while inflation is recently greater than 6%? Do you find traditional alternatives such as CDs or money market accounts similarly unattractive given interest rates 1% to 2% and long commitment periods greater than 1 year? Do you understand your […]

Which investment solutions that you own will perform well in an inflationary environment? At Essential Partners, we build portfolios for all types of economic environments, including rising inflation. Despite inflation being littered across the news and social media daily, the past 40 years have conditioned individual and institutional investors to not worry about inflation. This […]

What is your compass to traverse global financial markets and how does that translate to your portfolio? Do you own investments that perform well in all four economic environments? There are two core marcroeconomic variables that drive financial market changes; GROWTH and INFLATION. Consider a simple micro example as it relates to equities/stocks: Sales growth […]

Do you know that in 2 of the last 5 decades, stocks produced negative real returns vs. cash? What assets do you own that perform best in the decades when stocks perform worst? Do you own any assets that will perform well when inflation is high but economic growth is low? “Gold is money, […]

Investment portfolios that are balanced to various economic and inflationary environments will at times contain certain holdings with unrealized capital losses. Tax loss harvesting is a tactical portfolio strategy to sell these holdings to capture the capital losses, which can then be used to offset the capital gains realized elsewhere in the portfolio. Further, the […]

Do you know the true cost of your investment holdings? Does your salesperson/broker receive commissions? Does your salesperson’s firm capture any special distribution or marketing fees at your expense? Does your salesperson have sufficient training? Does your “robo-advisor” force you to hold too much cash? Warren Buffett’s partner Charlie Munger is famously outspoken regarding the […]

Do you have a disciplined process and documentation for your investment strategy? Does your salesperson/broker provide an Investment Policy Statement to set clear investment objectives, guidelines, and expectations? “Successful investment takes time, discipline and patience.” – Warren Buffett In our experience, no serious pension or endowment would invest without first creating an Investment Policy Statement. […]

Will your salesperson/financial advisor analyze investments they do not bring to you where they cannot earn fees or commissions? Has your salesperson/financial advisor ever thought your investment idea was a great idea if it meant you would be pulling the money from their control and fee structure? Has your investment advisor ever analyzed a company’s […]

Market Backdrop: 1/1/2026 to 3/31/2026

- Gold rose 8.4% during the quarter, with higher short-term volatility than the prior year

- The S&P 500 declined 4.4%, its weakest quarter since 2022

- International developed and emerging markets finished the quarter higher, returning 3.0% and 3.8%, respectively, and continued to outperform the S&P 500

- The U.S. dollar strengthened modestly, rising about 1.7%

- Oil was highly volatile, with Brent crude spiking sharply during the quarter amid geopolitical disruption

What is Different Right Now

Market volatility itself is normal. Pullbacks, rallies, rotations, and sentiment swings are part of investing. What is more unusual today is the speed at which narratives, priors, and regime expectations are being tested and revised. The headline cycle has its own rate of change. So does the geopolitical backdrop. So does the economic regime.

The discomfort many investors feel today is not just about market movement. It is about the fact that the assumptions underlying market movement are changing in real time.

That is true across economics, policy, technology, and geopolitics. Artificial intelligence is one example. AI is not a static theme investors can discount and move on from. It continues to evolve, forcing rapid reassessment of business models, productivity assumptions, competitive dynamics, labor implications, valuation frameworks, and market leadership. The same is true, in different ways, for trade policy, deficits, global alliances, inflation expectations, and monetary policy reactions.

Over the long run though, cash-flow producing assets, like stocks, ultimately follow earnings and cash-flow growth. In the short run, however, shifts in inflation, interest rates, policy, and investor expectations can drive meaningful changes in valuation and market leadership. That tension helps explain why markets can feel so unstable in the moment, even when the longer-term fundamentals matter most.

Before turning to positioning, it is helpful to ground the discussion in our Core Four framework.

The Core Four

Most market environments can be understood through one question:

What is happening to growth and inflation?

Rather than predicting a single outcome, it is more useful to recognize that markets rotate between regimes. Sometimes gradually, sometimes quickly.

The Last Six Years: Multiple Regimes, Not One Cycle

One of the clearest lessons from recent years is that we have not been living through one long, uniform bull market. We have moved through multiple regimes, and that matters because each regime rewards different investments and punishes others.

2020–2021: Goldilocks transitioning toward Reflation

What worked:

- U.S. growth stocks rose roughly 90% cumulatively over the period with technology leading

- Long-duration Treasuries rose 12% as measured by the 20+ year Treasury index

What was happening:

- Monetary policy support was strong, with the Federal Funds Rate dropping to 0.00%-0.25% and left there

- Massive liquidity entered the system: the CARES Act injected approximately $2.2 trillion, the Consolidated Appropriations Act added approximately $900 billion, and the American Rescue Plan added approximately $1.9 trillion

- Disinflationary assumptions still largely intact, at least initially, but that changed quickly with headline inflation rising from 2.3% to 7.2%

This was an unusually favorable environment for long-duration growth assets (once liquidity poured into markets and central banks backstopped assets). Investors were rewarded for owning the future, and the market put a very high value on future cash flows. But by 2021, inflation was already challenging the Goldilocks narrative. In hindsight, this period was less a pure Goldilocks regime than a transition from Goldilocks toward Reflation, even if price action had not fully caught up.

2022: A sharp shift into Stagflation

What worked:

- Energy stocks rose 59%

- Commodities rose 19%

- Gold rose approximately 12% in the first quarter, but sold off to end the year, down about -1% as real rates rose

What struggled:

- Growth finished the year down -30%

- Long-duration bonds were down -29%

- Speculative technology stocks were down -68%

What changed:

- Inflation continued higher with a peak year-over-year reading just shy of 9%

- The Federal Funds Rate rose from effectively 0% to 4.25%, sending the yield curve higher

- Liquidity conditions tightened as banks tightened lending standards, draining $1.2 trillion from the system

- The market repriced future earnings aggressively

This was the moment when the market violently rotated away from the assumptions that had dominated the prior cycle. The premium shifted from “future possibility” to “current cash flow, tangible assets, and scarcity.” In Core Four terms, this was a clear Stagflation shock.

2023–2024: Surface Goldilocks, underlying mixed regime

During this period, the environment was more mixed. At the index level, markets often looked healthy. Large-cap benchmarks advanced, and the dominant interpretation became that the economy had stabilized, inflation had moderated, and the old growth leadership was reasserting itself. But under the surface, the picture was less simple.

What we saw instead was:

- The S&P 500 Equal Weight Index lagged the market-cap-weighted S&P 500 by roughly 30 percentage points

- Mega-cap stocks drove a disproportionate share of index returns, with that cohort up roughly 65%

- Market breadth was uneven, with leadership concentrated in a relatively narrow set of names

- Real assets were mixed, with commodities down approximately -1% and gold up 42%

- Inflation was moderating but not disappearing. Headline CPI averaged 3.6% on a year-over-year basis

While the surface narrative resembled Goldilocks, the underlying reality looked more like a Goldilocks/Stagflation overlap. That distinction matters. It means the market was not broadly endorsing a single, unambiguous macro outcome. It was rewarding a narrow set of dominant winners while still favoring some inflation-sensitive investments underneath.

2025 through Q1 2026: Reflation bias with Stagflation risk

That brings us to today.

The current backdrop looks less like a return to old-style Goldilocks and more like a Reflation / Stagflation blend.

The broad message from recent market leadership has been:

- Real assets remain firm with commodities up 39%

- Gold remains strong, up 75%

- Energy stocks have appreciated 47%, outperforming technology stocks by 32%

- Select value and cash-flow-oriented investments are holding up better than growth stocks, outperforming by about 2%

- Long-duration bonds are normalizing, returning only approximately 4%

- Geographic dispersion remains high, with international developed and emerging markets outperforming the S&P 500 by 21% and 27%, respectively

Translation: economic growth has not collapsed, but inflation has not disappeared either. Policy remains mixed. Trade, deficits, geopolitics, and fiscal dynamics continue to complicate the path forward.

That is not a uniformly supportive Goldilocks environment. It is an inflation-sensitive environment where both careful equity selection and real assets can work, but the balance remains fragile.

Why This Is More Volatile Than “Normal Volatility”

Part of what investors are experiencing today is not just normal market volatility. It is the higher rate of change in the inputs.

We are constantly reassessing:

- inflation assumptions

- interest rate assumptions

- growth assumptions

- geopolitical assumptions

- technology assumptions

- policy assumptions

The result is that market priors are being stress-tested and altered more rapidly than usual.

Prior assumptions about globalization are being tested.

Prior assumptions about disinflation are being tested.

Prior assumptions about U.S. exceptionalism, interest-rate sensitivity, and market concentration are being tested.

Prior assumptions about productivity, labor, and technology adoption are being challenged almost daily, particularly by AI

That does not mean markets are broken. It means the half-life of consensus is shorter.

So What Now?

The most common question we’ve received is straightforward: What should investors do now? More specifically, should recent volatility lead to changes in portfolio strategy, particularly in areas like gold and other inflation-sensitive assets?

Our view is that recent market volatility, by itself, does not invalidate the broader portfolio framework. If anything, it reinforces the importance of owning a portfolio built for multiple economic outcomes rather than one narrow market narrative.

That is especially true in an environment where the rate of change in assumptions remains high. Investors are not just reacting to earnings, inflation prints, or central bank commentary. They are also repricing the likely path of fiscal policy, geopolitical risk, global trade, technological disruption, and the durability of prior market leadership.

Gold is a useful example. It has been a strong performer over recent years, and with that strength has come higher short-term volatility. That should not be surprising. Assets that provide meaningful diversification often do not move in straight lines, especially after strong advances. Periods of consolidation or pullback are normal.

More importantly, the strategic case for gold remains intact. Gold has historically been most helpful in environments where traditional financial assets struggle, expectations are reset lower, or inflation remains elevated while growth weakens. In other words, it has tended to matter most in deflationary stress and stagflationary regimes, which is precisely why we continue to view it as a useful diversifier rather than a tactical trade.

History provides a useful reminder. In the 1970s, stocks underperformed cash, while gold compounded at roughly 31% annually. From 2000 to 2010, stocks again underperformed cash, posting a negative absolute return over the decade, while gold returned more than 14% annually. The lesson is not that gold always wins. It is when stock-heavy portfolios go through long stretches of disappointment that gold has historically been one of the few assets capable of offsetting that pain.

That is particularly relevant today. We are not operating in a straightforward Goldilocks environment where broad stock market investments alone can be relied upon to do all the heavy lifting. We are in a market where inflation has proven stickier than many expected, policy remains messy, leadership is narrower than headline indices suggest, and macro assumptions are being revised quickly. In that world, diversification is not a theoretical exercise. It is a practical necessity.

So what now? For us, the answer is not to chase every move or overhaul portfolios in response to short-term volatility. It is to stay disciplined and continue emphasizing a structure that can adapt across regimes:

- Selective equity investment, rather than blind dependence on broad index concentration

- Real assets, including gold and commodities, as portfolio ballast in inflation-sensitive environments

- Liquidity and shorter-duration fixed income, where appropriate, to preserve flexibility and pounce when opportunities elsewhere arise

- Diversification across both global markets and economic outcomes, rather than reliance on a single macro forecast

The goal is not to predict each short-term move correctly. The goal is to own assets that can respond differently as the environment changes. In a world where assumptions are shifting faster, that discipline matters more, not less.

In a world defined by rate of change, diversification is not a luxury. It is the starting point.

Thank you for your continued trust and support.